(Bloomberg) — Bank of America Corp. joined its largest rivals in setting aside more reserves as a growing number of consumers couldn’t keep up with their loan payments, even as executives dialed down fears of a looming crisis.

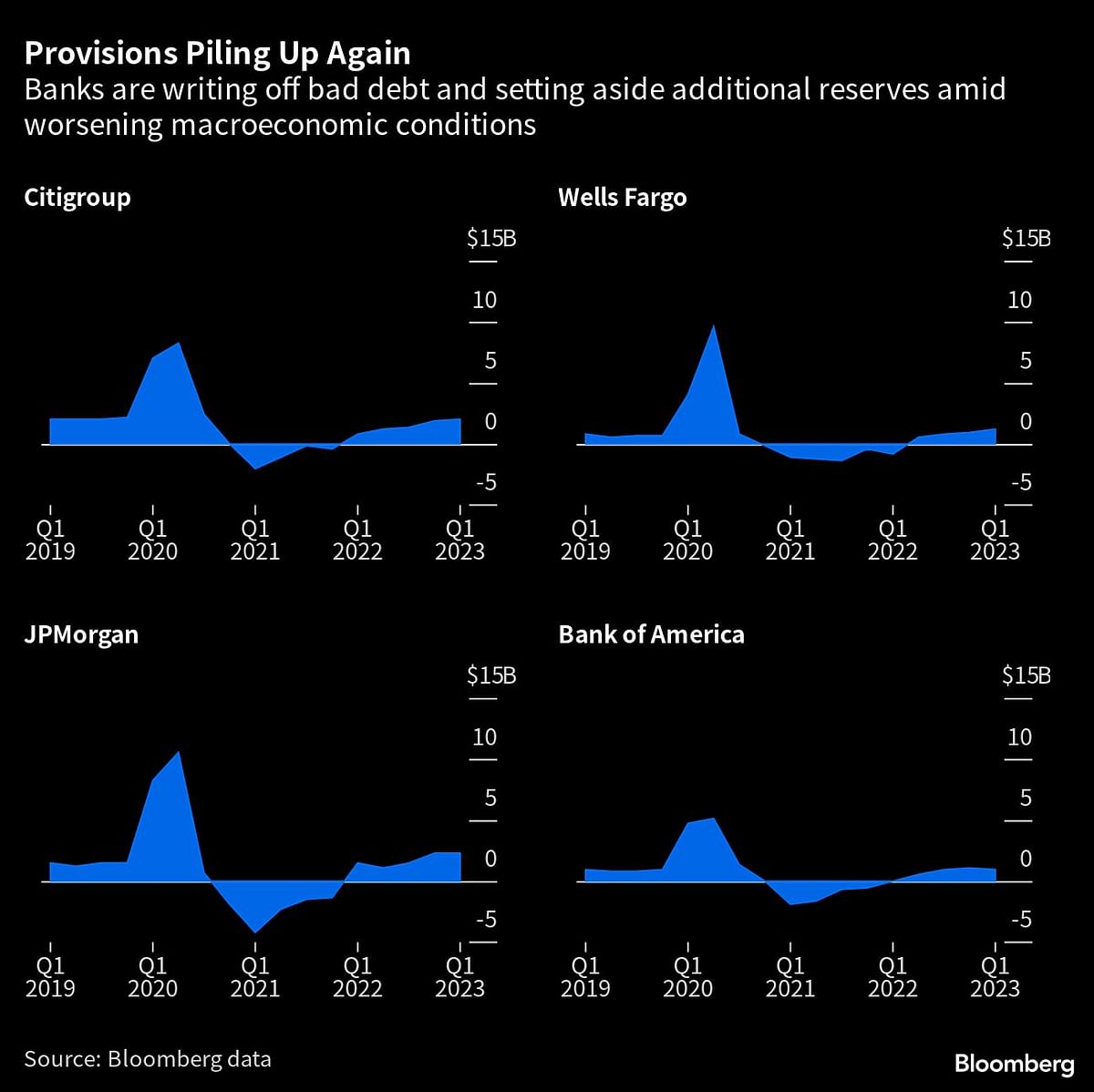

The four biggest US lenders wrote off a combined $3.4 billion in bad consumer loans in the first three months of 2023, a 73% increase from a year earlier. That, combined with additional reserves, boosted provisions at all four institutions to levels not seen since the earliest days of the Covid-19 pandemic.

For years, banks benefited from the financial strength of US consumers as credit losses fell to record low levels. Now, with once-in-a-generation levels of inflation whittling away at their savings, Americans are once again beginning to fall behind on payments.

But so far, bank executives have been adamant that the recent increase in provisions is nothing more than losses returning to normal after pandemic-era government stimulus programs kept consumer defaults artificially low.

“We haven’t seen any cracks in that portfolio yet,” Bank of America Chief Financial Officer Alastair Borthwick said Tuesday on a conference call with reporters. “The consumer is in great shape.”

At Charlotte, North Carolina-based Bank of America, firmwide provisions were less than expected, helped by reserve releases tied to corporate loans, according to a statement. Still, the firm was forced to set aside an additional $360 million in reserves tied to its consumer business, which the bank blamed on higher than expected credit-card balances.

At Goldman Sachs Group Inc., the platform-solutions division that includes the firm’s burgeoning credit-card effort saw provisions soar to $265 million in the quarter. The Wall Street giant partly blamed the increase on a rise in net charge-offs for its credit-card portfolio.

Wells Fargo & Co. chalked up its $1.2 billion in provisions to higher net charge-offs in both consumer and commercial loan portfolios. The San Francisco-based company said Friday that it’s begun to tighten underwriting standards for credit-card loans as it seeks to position its debt portfolio for a slowing economy.

“We continue to see some gradual weakening in underlying credit performance, including higher nonperforming assets,” Chief Financial Officer Mike Santomassimo said on a conference call with analysts. “We are proactively monitoring our clients’ sensitivity to inflation and higher rates and are taking appropriate actions when warranted.”

JPMorgan Chase & Co., the world’s largest credit-card issuer, said bad card loans soared to $922 million in the first quarter, up 82% from a year earlier. The 30-day delinquency rate on those loans — a harbinger for future losses — climbed to 1.68% from 1.09% a year earlier.

Still, executives at the New York-based bank said they’re not taking drastic action in response. Rather, the firm is focused on fine-tuning its real estate portfolio as investors increasingly worry about rising losses on office loans.

“I wouldn’t use the word credit crunch,” CEO Jamie Dimon said on a conference call Friday. “Obviously, there’s going to be a little bit of tightening and most of that will be around certain real estate things.”

Citigroup Inc. reassured investors Friday that the increased credit losses in the first quarter were completely expected. CEO Jane Fraser said the New York-based bank is relying on a vast trove of data to keep track of consumers who borrowed money from Citigroup and how they’re handling their debt obligations.

“We can’t just rely on FICO scores for assessing the credit of our customers and our portfolio,” Fraser said. “There is a tremendous amount of data that we draw upon that goes well well beyond that and that’s also, as you can imagine, something that gives us a lot more confidence.”

{kind=link}